It's the implied, non-inflationary price of gold in a system where you have either a gold system or some reference to gold. Now, there's not a central bank in the world that wants the gold standard, but they may have to go to it — not because they want to, but because they have to — in order to restore confidence in some sort of future financial crisis. The problem right now is that central banks have not normalized their balance sheet since 2009. They're trying, but it's not even close.

If we had another crisis tomorrow, and you had to do QE4 and QE5, how could you do that when you're already at $4 trillion? They might have to turn to the IMF or SDR or to Gold.

Then, if you go back to the gold standard, you have to get the price right. People say there's not enough gold to support a gold standard. That's nonsense. There's always enough gold, it's just a question of price. Take Japan, Europe, China and the US — the big four economies — their m1 is approximately $24 trillion. If you had 40% gold backing, that would be $9.6 trillion. There are about 33,000 tons of official gold in the world. So you just divide 9.6 trillion by 33,000 tons and what you get is about $10,000 an ounce.

Then, if you go back to the gold standard, you have to get the price right. People say there's not enough gold to support a gold standard. That's nonsense. There's always enough gold, it's just a question of price. Take Japan, Europe, China and the US — the big four economies — their m1 is approximately $24 trillion. If you had 40% gold backing, that would be $9.6 trillion. There are about 33,000 tons of official gold in the world. So you just divide 9.6 trillion by 33,000 tons and what you get is about $10,000 an ounce.

If you had a gold standard with a lower price, that would be deflationary. You'd have to reduce the money supply. That was the mistake that was made in 1925. It did contribute to the Great Depression, and it wasn't because of gold, it was because they got the price wrong. So to have a gold standard today and not cause another depression, you'd have to have a price around $10,000 an ounce.

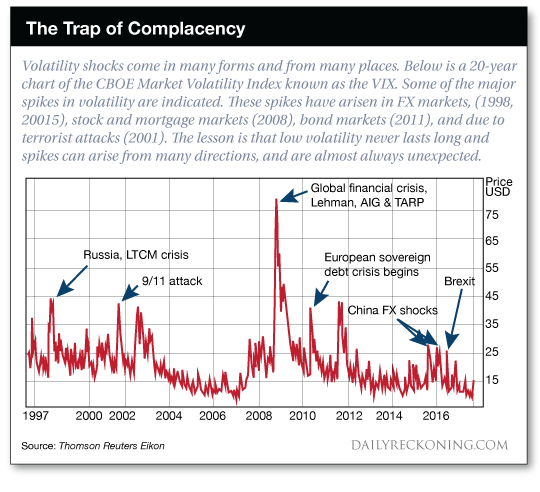

- Source